Great Britain’s overall energy picture: As highlighted in the market summary, during the second quarter, Great Britain became a net exporter of electricity for the first time, with net exports totaling 3.6 TWh. This flip in net interconnector flow direction is attributed to three main factors:

- There were substantial cuts in natural gas supplies to Europe from Russia as a result of international tensions stemming from Russia’s invasion of Ukraine. This has led to high gas prices across the continent.

- There were increased levels of liquefied natural gas (LNG) exports to mainland Europe and Ireland, but Great Britain has had to deal with limited gas connection capacity with its neighbors and a long-term decline in gas storage capacity. These issues led to an “excess” of gas—and lower gas prices—in Great Britain, compared with the rest of Europe.

- There was reduced energy availability from the French nuclear fleet, increasing Europe’s demand for energy from Britain.

Nuclear and Great Britain: The predominantly outward flow of electricity from Great Britain to mainland Europe in the second quarter was partly “driven by stress corrosion cracking in some units in the French nuclear fleet, which decreased supply and further increased the need for French imports from GB,” according to Paul Verrill, director of EnAppSys.

The report notes that nuclear output in Britain was higher in the second quarter, at 12.14 TWh, than in any quarter since the fourth quarter of 2020, when nuclear output was 13.43 TWh.

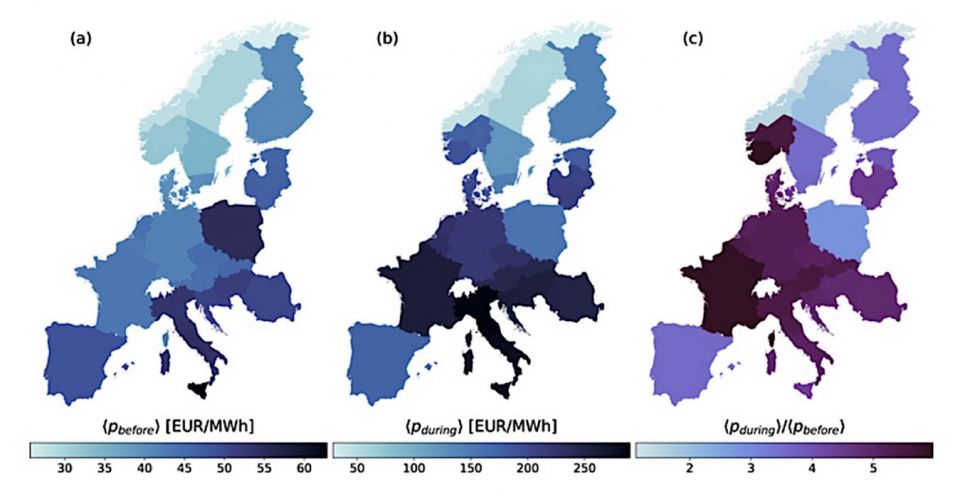

Europe’s overall energy picture: In its report for mainland Europe, EnAppSys notes that on the Continent, as in Britain, the Ukraine conflict has led to reductions in natural gas supplies from Russia and sparked uncertainty regarding future supplies, resulting in record-high gas prices during the second quarter. Wholesale gas prices, which have more than doubled since the previous year, has caused much distress in the European Union’s energy market.

Because of the cuts in gas supplies from Russia, Europe “has accelerated plans for renewable development and increased levels of LNG capacity,” said Jean-Paul Harreman, director of EnAppSys BV in The Netherlands. Europe saw high levels of gas and coal/lignite generation in the second quarter, as well as record levels of wind and solar power generation. According to the report, “nuclear output fell further than the levels in Q1 due to France continuing to see more unprecedented levels of unplanned outages in the nuclear fleet.”

Nuclear and Europe: In terms of Europe’s nuclear energy market, “French nuclear output has been in a continuous decline since the end of January, with 7.5GW going off line over February and 12.9GW going off line over March for maintenance. The continued decline into Q2 2022 has put added pressure on the European wholesale market since France has always been the primary exporter in Europe,” according to the report. As Harreman explained, “The well-documented technical issues in the French nuclear fleet caused a change in interconnector flows and France also became a net importer during the quarter.”

Statistics cited in the European Electricity Generation Summary reflect the slowdown in French nuclear output. Europe’s total nuclear energy generation in the second quarter of 2022 was 146.4 TWh, compared with 190.2 in the first quarter of this year and 174.6 in the second quarter of 2021. Despite the problems with the French nuclear fleet, the report points out that nuclear power was still the biggest contributor to Europe’s fuel mix during April–June 2022, generating 22.7 percent of the total energy output, compared with 18 percent for natural gas, 16 percent for hydro, 15.3 percent for coal/lignite, 14.9 percent for wind, 8.8 percent for solar, 3.3 percent for biomass, 0.5 percent for waste, 0.3 percent for oil, and 0.2 percent for peat.